Worst time to start trading?

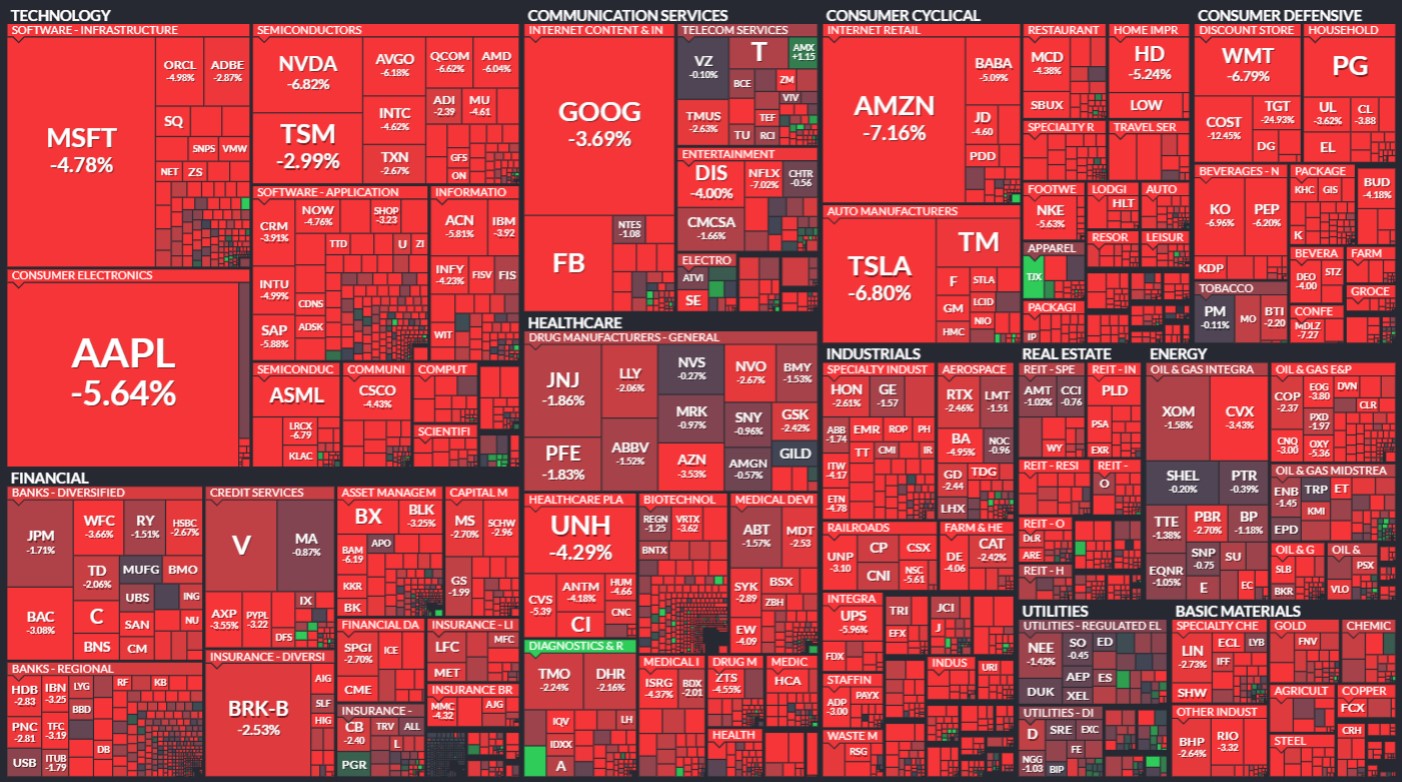

Four months and a half in my equities trading experiment and this is how the market looks. If you are not familiar with this kind of chart, it's the day's full chart of US companies from FinWiz. Red means that a square goes down, green that it goes up. My "portfolio", meaning my assorted stock that I created buying every month since the beginning of the year, is now 20% less valuable. This sounds bad, but it is even worse, since at the beginning of April it had not lost any value.

I did not invest much, so I can only imagine the pain people feel when their portfolio is actually their savings and this happens. To me it's a game, to others it's life and death. And I know that in theory if you put all your money in stock, then you did it wrong, but it can't feel good. And now it's almost certain that a recession is coming, possibly a "stagflation", which is the finance sector's version of "Everything Everywhere All at Once". Sorry, I couldn't help it, since I've just watched that film. It was good. Also, very on point, I now realize.

So what do you do when everything seems stacked against you? Well, why ask me? Haven't you read above? I am playing at trading and watching movies instead of learning to do it better. But I will tell you anyway, because that's the kind of person I am.

Here is what has been going on the last few months.

First, the market started to lose steam from its heights in November, mostly because the United States stopped the "money printing" they used to handle Covid. Typical Americans, right? First try to blow it up, then they throw money at it. If you don't know what that means, the Biden administration pushed for trillions of dollars to be poured into the economy as the country was at a viral standstill. It may have been a bad choice, but I believe it wasn't the worse and possibly it was the only one they had. But now that the Covid pandemic is "gone", the money went away and it basically burst a bubble. In the U.S. there is the lowest unemployment since forever, but also the highest inflation. So their Federal Reserve started to increase interest rates, taking the steam from the growth of the country, basically.

Secondly, Covid itself did some damage to the global economy, rising tensions, making people crazier than usual - and that's saying something, but also disrupting the supply chains. These are the connections that countries, corporations and people have created over the decades in order to keep functioning. All this on the basis of past experience, where circulation of people and produce was relatively cheap and easy all over the planet. Not anymore! Every day we now hear of shortages of material and people. What that means is that you have a producer of something, be it material or service, and you have a buyer that is interested in it. When you have both demand and offer, you make money. Not this time! Because the producer can't produce things fast enough to cope with demand. They've "streamlined" their business for so long they can only do it one way and that way is gone.

Then, some Russian decided Ukraine was a nice toy and went for it. I don't know if you've heard of that. And everybody else decided they didn't want to have anything to do with Russia. It so happens that Russia and Ukraine are the main suppliers of raw material in a lot of economic sectors, including grain and natural gas. I guess it is an important moment to take stock (pun not intended) at how important these countries are for the planet (as well as many others that we've ignored because they are not in the spotlight). What that leads to is more shortages, which leads to price increases for the remaining sources of material. A minor thing to add here is that one of the supporters of Russia, at least partially, is China, a great supplier of work and material.

It's the perfect storm, yet most people still cling to the status quo they've had for possibly the entirety of their lives. Every low in the market is now a dip to buy even when the market keeps going lower. And lower. And lower. Every temporary high of the market is a bullish rally that will get us out of the situation. In case you didn't know the financial industry is at balance with nature, so everything is named after some animal: bulls, bears, hawks. It's like King-Fu, but with money! Every new startup is the savior of the market with their technology that will solve everything. And then there are the charts. People love to read the charts, like leaves in tea, and predict the future. They give pet names to patterns in the charts, they make analogies to things past, they criticize others and delight in their own perfect strategy for the future.

Only it's not that easy. There are money in the world, but they can't move. There are people in the world, but they are sick, at war or falling prey to opportunistic governments that use this moment of weakness to get the worst out of people. Old strategies (well, not that old, but an eternity from the viewpoint of a day trader) don't work anymore because the situation is different. This time, I am afraid, it really is very different.

Let's look at some investing strategies

First of all, everybody knows, when the market starts to fall, you sell the "growth stocks", meaning you stop betting that some companies will have a sudden growth spurt like tech companies and "disruptors", and you buy more stable things, like bonds. Perhaps you still want to keep stock, but you choose the safer ones: oil, retail, real estate. A lot of people did that and were wallowing in schadenfreude watching other still cling to their belief this was a temporary lull in the market. But then major retail companies like Target and Costco fell 12% in one day. Why? Because money is losing value (inflation), products are shit (supply chain disruption) and there is no energy to improve on them (stagnation).

Because of the Russian conflict, oil is through the roof right now. Oil is still good, if you bought it early, but if you buy it now it will keep at the same price for a while, then drop. Funny enough, this will lead to an explosion of renewables, but not immediately because they don't have the rare and specialized material they need to build it. As for real estate, that still works for now, but for how long? People will start losing jobs, their money lose value and with the entire economy down, they will not find estate buyers or renters either.

What about bonds, then? As I was saying, the Fed is increasing borrowing interest rates to stave off inflation. Bonds have an inverse relationship with interest rates. There.

What about utilities?! What about energy? What about Big Pharma?!

I could write on and on, but first of all I am not that good (have you read this far?!) and second it's simple: if there is less energy in the system, the system will slow. Probably pharmaceuticals are a good bet, because no matter how poor you are, health is important. But watch out, because a lot of companies rose to prominence lately on their work against Covid. With less Covid, these companies will still do well, but they will lose from their overall value. So you get in a situation where you kind of wish everybody has Covid except you... I personally think that's very funny, but I have a weird sense of humor.

What about money, then? Just keep the money in the bank. That's safe, right? Well, yes. It's safe, but during rampant inflation, what you see is that money is losing value. Same thing as with house renting. You maybe get enough to counteract inflation, but just that. Gold would work, but it's cumbersome, unsafe to hold and it's already pretty high because for a while everybody wanted to have it just in case the war expands. It might still do. You buy it now, it might deflate later.

There are things one can do, like "alternative investing". I couldn't tell you exactly what that means. Being alternative means they are like plan B when everything else fails. It sounds the right direction, but what should you choose? There are for example some platforms that allow you to invest in art, like you buy 10% of a painting. Or stuff like hedge funds, which is an entirely different can of worms. Or even private equity, which makes you more of a company partner than just buying publicly traded stock because only a few people have access to it, like the founders.

The end of investing?

Best strategy: sell your investments and start drinking it away! No. That doesn't really work, either, as fun as it sounds. In fact, investing is a good strategy at any moment. Yes, those are bold letters. Investing is the opposite of spending or, at best, doing absolutely nothing. For example learning new skills is investing, too, and maybe the best possible kind. But I am not here to tell you to grow up, so let that go for now. Spending some money, though, is not a bad idea. For example one could use some money to go on some cheap vacation or buy something that makes them happy. When nothing has value, everything does, right?

The problem with stagflation is that value goes down and then there is a plateau where nothing happens. If that is coming next, then you can buy stock at any time during the plateau and you see no result for years. If you buy too early, the market can still go lower and you lose. And we're not even sure a stagflation is coming, which means you don't know exactly when to find that sweet spot to buy, either.

But the silver lining is that you don't have to. The fact that companies went down is actually an opportunity. The only problem is that it's long term. No matter when you buy: now or further down the line, their value is guaranteed to come up. At some time. Four months and a half is not long term, decades is long term. That is why you don't keep all your savings in stock, either. You have cash for short term.

Does this period hurt investors? Hell, yeah. Especially if you started in November and not in January like me... Suckers! It is even more painful when you started somewhere in 2020 and you saw everything explode and go up and up and up, just to see it all crashing down again. And it all feels hopeless and you had dreams and you got just a little too greedy and if you had just exited at the right time and so on and so on. It's all bullshit. No one could have predicted this with any significant accuracy. Unless it's your job, losing money on the stock market is just normal. It's all chaos. What is not chaos is finding some companies that you trust (to not implode and disappear, like Blockbuster or Nokia, and to continue growing) and stick with it. Investing is not about winning, but about growing. Winning implies a moment in which it happens, but growing is a continuous process.

So no, it's not the end of investing, it's barely the start. These things happen and in the large scheme of things they are merely blips. The general principle remains: you either trust humanity goes forward or you don't. In the first case, you're an optimist, life is always ahead of you and investing is the rational thing to do. On the average it just goes up. In the second case, you're a grouch! Why continue living if the best of everything is behind you? On a more metaphorical level, every second of life is a compound investment.

What I wanted to convey in this post is that you have to thread carefully because there is a lot of shit happening, but it certainly not the end of the world... or is it? Ta da daaaaaam!